Is your business equipped to take on the challenges that come with a new tax year?

On 6th April, the 2021/22 tax year began – and accountants have labelled it ‘the busiest ever’ in terms of tax.

In this article we have compiled the highlights and major changes likely to have an impact on your business in this new tax year, such as:

- Wage & salary,

- Corporation tax and capital allowance,

- VAT rates,

- Miscellaneous taxes,

- Brexit tax,

- Coronavirus tax,

- And finally – IR35.

A lot to consider! So, let’s get stuck in…

Wage & Salary Changes

As expected, minimum wage amounts, and personal tax and National Insurance allowances have seen a slight boost for 2021/22. There have also been adjustments to the National Living Wage and the National Minimum Wage.

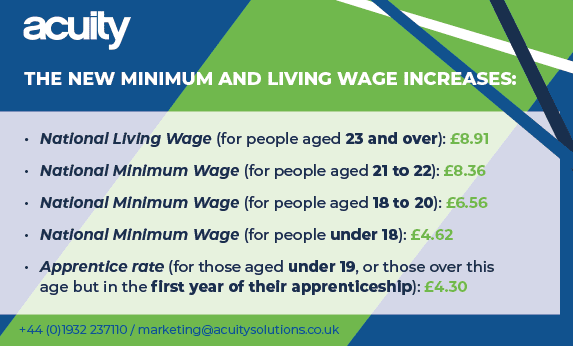

Minimum & Living Wage Amounts

Since April 2021, the minimum wage you pay employees has increased.

New to the 2021/22 tax year is that the National Living Wage is available to 23 & 24-year-olds for the first time, having previously been limited to those aged 25 and older.

Income Tax Personal Allowance

On April 6th we saw a slight increase to personal allowance and higher-rate thresholds for the coming year. These amounts – I’m sure you have already heard through media and online discussion – have actually been frozen until April 2026!

The income tax bands for the new tax year are as follows:

- Personal allowance: Up to £12,570 (0% tax rate)

- Basic rate: £12,571 to £50,270 (20% tax rate)

- Higher rate: £50,271 to £150,000 (40% tax rate)

- Additional rate: More than £150,000 (45% tax rate)

National Insurance Contributions

National Insurance contributions (NICs) rose in a similar way for 2021/22, with the Class 1 NICs (Primary Threshold/Lower Profits Limit) rising to £9,568.

However, with the exception of the Upper Earnings Limit (UEL)/Upper Profits Limit (UPL), discussed below, this and other NICs are not pegged until 2026.

They may rise “at future fiscal events”, to quote the government’s budget announcement.

The Upper Earnings Limit (UEL)/Upper Profits Limit (UPL) rises to £50,270 to match the afore mentioned higher-rate threshold for income tax. And, like that increase, it’s also pegged until April 2026.

Changes in corporation tax & capital allowance

Do you want the good or bad news first? …

Corporation Tax

Let’s start off with the good news. There is no increase in corporation tax for the 2021/22 tax year, and there will almost certainly not be one in the 2022/23 – PHEW!

But the bad news is… all that changes in in April 2023 when we can expect to see the first rise in corporation tax since 1974!

Corporation tax is set to rise to 25% on profits over what will then be labelled as an Upper Profits Threshold of £250,000.

This shouldn’t have too much of an impact on smaller businesses – those with profits under £50k will benefit from a Small Profits Rate, meaning their corporation tax rate will remain at 19% as of April 2023.

However, for those larger businesses, from April 2023 there will be a new tiered corporation tax rate system in place for those of you with profits between £50k and £250k. Though the Government are yet to reveal the details of this new tiered system, so look out for that one!

Capital Allowance

Some more good news before we stress you all out…

There is a new super-deduction capital allowance (set at 130%) that can be used between 1st April 2021 until 31st March 2023.

So, if your company is looking to invest in qualifying new plant and machinery assets, you can not only claim back the cost as a first-year capital allowance, but also receive 30% on top of that.

This is basically like the Government paying you to buy assets – their way of encouraging firms to invest and achieve growth.

There’s also a further capital allowance measure that can be used by investing companies, who benefit from a 50% first-year allowance for qualifying special rate (including long life) assets.

VAT Rates

VAT rates haven’t changed for this new tax year, with the exception of Coronavirus relief measures aimed at hospitality sectors (discussed below).

The VAT threshold also doesn’t change from £85,000 and is frozen until 1st April 2024.

Miscellaneous taxes

Although not directly related to business, it’s worth mentioning that the following personal tax allowances/thresholds don’t see an increase in 2021/22, and are also frozen until April 2026:

- Inheritance tax thresholds

- Pension’s lifetime allowance

- Capital gains tax annual exempt amounts.

Brexit Tax

Due to Brexit, January 2021 brought changes in the way VAT is handled for imports in the form of postponed VAT accounting.

Though, Brexit legislation doesn’t directly change any other kind of business tax, so no changes across the 2021/22 financial year.

Coronavirus tax measures

One of the biggest recent changes in the tax world is of course down to the dreaded C-word – Covid-19, of course!

Those in the hospitality sector have seen a reduced VAT rate of 5% since July 2020. This was due to end on 31st March 2021 but has been extended further until 30th September 2021. After this, a new 12.5% rate will be applied until 31st March 2022, then the usual 20% rate will resume from 1st April 2022.

Flat rate VAT users in the hospitality sector also receive some relief from the flat rate scheme -reductions include:

- Catering services: 4.5% until 30th September 2021, and 8.5% following this until 31st March 2022.

- Hotel and accommodation: 0% until 30th September 2021, and 5.5% following this until 31st March 2022.

- Pubs: 1% until 30th September 2021, and 4% following this until 31st March 2022.

- Lastly, although not new in the 2021 Budget, it’s worth noting that the government have opened the portal for the New Payment Scheme for VAT deferral amounts.

IR35 Changes

The new tax year has brought changes to how medium and large businesses are required to manage the tax matters of contractors whom they employ.

This has been labelled as Intermediaries Legislation, or ‘the off-payroll working rule’, but best known as IR35.

In summary IR35 is intended to identify ‘disguised employees’, or ‘deemed employees’ as some may prefer.

These are contractors who work at a company in the same way that full-time employees do, but the work is defined by a contractual agreement and the contractor invoices for hours worked through a third-party agent, which is often a personal services company (PSC).

The change here is that medium and large businesses must now determine if the IR35 apply to contractors they hire. If so, they are required to pay a Deemed Employment Payment – essentially, ensuring the contractor pays the same amount of tax compared to a regular employee.

Tax less taxing with Sage & Acuity

We know these changes can be hard to get your head around, so we hope we’ve helped to clarify things!

Although, even if you understand, it can still be difficult to implement these changes into your business and ensure compliance…

…unless of course you have a finance system in place that has the power to make tax easy!

Acuity and Sage have extensive experience of working with British businesses and accountants.

Sage is a HMRC-trusted product, and they have worked together for years to ensure their accounting products are leading the way in compliance.

Avoid having to change numerous spreadsheets every year, submit tax returns with confidence and rest assured that your business is 100% compliant, with Sage software.

Acuity can help you on this journey to a more efficient financial system. Whether you need Sage Intacct or Sage X3 we can offer you full support and guidance through implementation and beyond. More so, we are the only UK partner to offer fixed price implementation as standard, so no surprise costs to trip you over!

Visit our product pages for more information, or get in touch!